Retirement Alert: 3 Pitfalls Of Relying Solely On Social Security For Lifetime Income

Are you counting on Social Security to provide a lifetime income in retirement? You're not alone. According to the Social Security Administration, over 70% of Americans rely on Social Security as a primary source of income in retirement. However, this reliance can be a recipe for disaster. Relying solely on Social Security for lifetime income can lead to a host of problems, including reduced living standards, increased poverty, and even bankruptcy. In this article, we'll explore three pitfalls of relying solely on Social Security for lifetime income and provide strategies for mitigating these risks.

The Social Security System: A Flawed Safety Net

The Social Security system was designed to provide a basic level of income support for Americans in retirement. However, the system is based on a flawed assumption that workers will live longer and work longer than they actually do. As a result, the system is facing a funding crisis, with the Trust Fund projected to be depleted by 2035. Furthermore, the system's benefit structure is based on a percentage of previous earnings, which can result in reduced benefits for higher-earning workers.

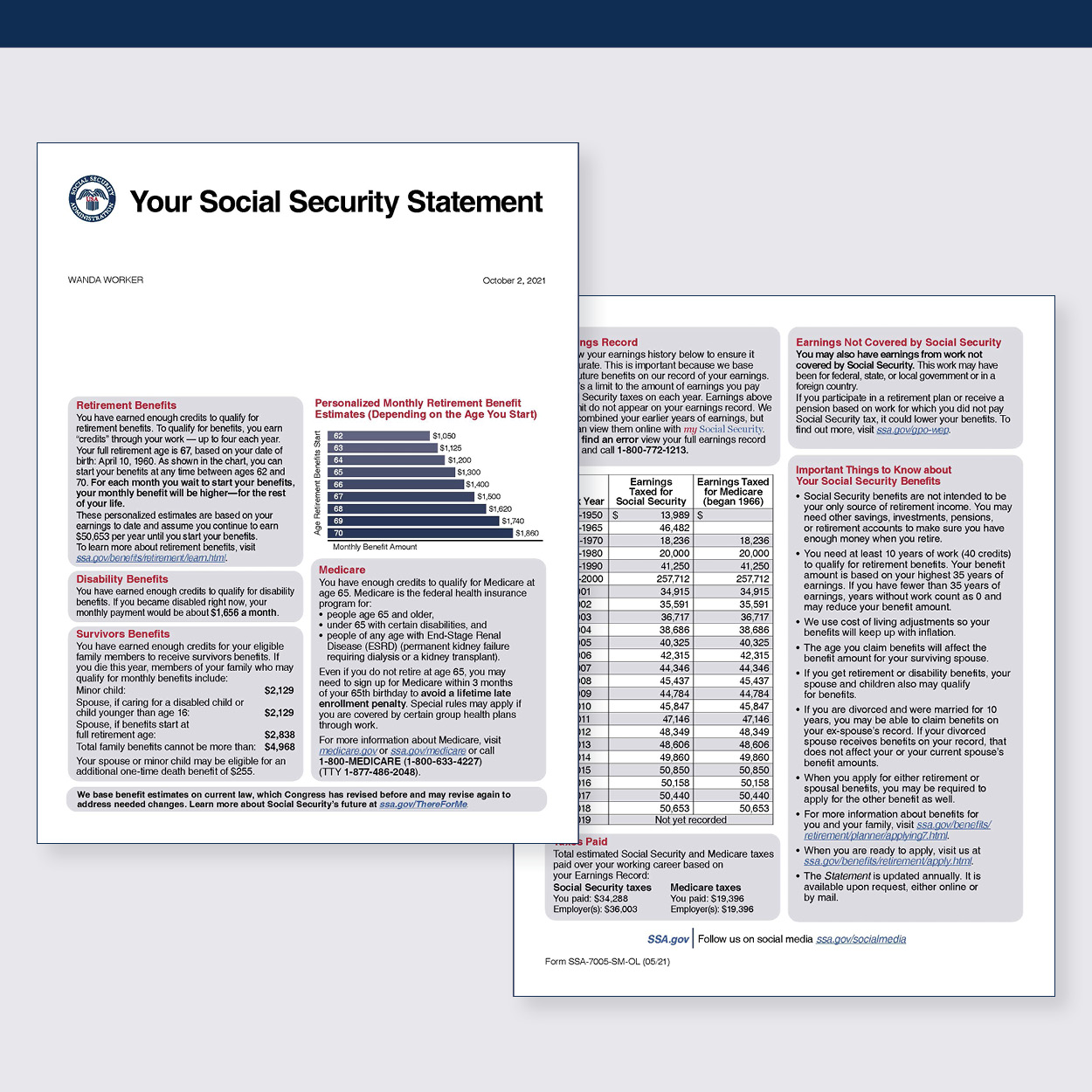

How Social Security Benefit Calculation Works

The Social Security benefit calculation is based on a formula that takes into account a worker's 35 highest-earning years. The benefit amount is then adjusted based on the worker's age at retirement. This means that workers who retire earlier will receive lower benefits, while workers who delay retirement will receive higher benefits. However, this formula can also result in reduced benefits for workers who earn higher incomes.

Pitfall #1: Reduced Living Standards

Relying solely on Social Security for lifetime income can result in reduced living standards for retirees. According to a report by the Employee Benefit Research Institute, 63% of retirees live on 50% or less of their pre-retirement income. This means that many retirees have to make significant lifestyle adjustments in order to make ends meet. Furthermore, this reduction in living standards can have long-term consequences, including increased health problems and decreased longevity.

Strategies for Mitigating Reduced Living Standards

One strategy for mitigating reduced living standards is to increase retirement income through other sources, such as a 401(k) or IRA. This can help to supplement Social Security benefits and increase overall retirement income. Additionally, retirees can consider working part-time or taking on a side hustle to increase income and offset the cost of living.

Pitfall #2: Increased Poverty

Relying solely on Social Security for lifetime income can also result in increased poverty among retirees. According to a report by the Social Security Administration, over 15 million Americans receive full or partial benefits from Social Security. However, this means that many retirees rely on other sources of income, such as pensions or savings, in order to make ends meet. This can result in increased poverty rates among retirees, particularly among those with lower incomes.

Strategies for Mitigating Poverty

One strategy for mitigating poverty is to increase retirement income through other sources, such as a pension or retirement account. This can help to supplement Social Security benefits and reduce reliance on government support. Additionally, retirees can consider pursuing education or training to increase earning potential and improve living standards.

Pitfall #3: Bankruptcy and Financial Ruin

Relying solely on Social Security for lifetime income can also result in bankruptcy and financial ruin for retirees. According to a report by the National Foundation for Credit Counseling, over 8 million Americans have filed for bankruptcy in the past year. Many of these filers were retirees who relied on Social Security benefits to make ends meet. This can result in significant financial consequences, including loss of assets and reduced credit scores.

Strategies for Mitigating Bankruptcy

One strategy for mitigating bankruptcy is to increase retirement income through other sources, such as a retirement account or part-time work. This can help to supplement Social Security benefits and reduce reliance on government support. Additionally, retirees can consider creating a budget and prioritizing expenses in order to manage finances more effectively.

Conclusion

Relying solely on Social Security for lifetime income can be a recipe for disaster. The system is flawed, and relying on it for income can result in reduced living standards, increased poverty, and even bankruptcy. However, by increasing retirement income through other sources and pursuing strategies for mitigating these risks, retirees can reduce their reliance on Social Security and improve their overall financial well-being.

Recommended Strategies for Retirees

• Increase retirement income through other sources, such as a retirement account or part-time work.

• Pursue education or training to increase earning potential and improve living standards.

• Create a budget and prioritize expenses in order to manage finances more effectively.

• Consider consulting with a financial advisor to develop a personalized retirement plan.

What You Can Do Now

Take the first step towards securing your retirement income today. Consider increasing retirement income through other sources, such as a retirement account or part-time work. This can help to supplement Social Security benefits and reduce reliance on government support. Additionally, create a budget and prioritize expenses in order to manage finances more effectively. By taking these steps, you can reduce the risks associated with relying solely on Social Security for lifetime income and improve your overall financial well-being.

Recent Post

Unlocking The Secrets Of Menopause: Expert Insights On Navigating Life After 40 With Paolo Tantoco

Tensions Rise As Trump Officials Defend Tariffs Amid Market Volatility And Warnings For Savers And Retirees

Rosie O'Donnell Teases Trump Move, Posts Disruptive Selfie From Abroad

Wings For The Win: Capitals Edge Ducks 7-4 In Thrilling Matchup

Ducks Fall Short: Key Takeaways From Thrilling 7-4 Loss To Capitals

Article Recommendations

- Unveiling The Enchanting World Of Chloandmatt: A Journey Into Love, Adventure, And Inspiration

- Explore The Enchanting World Of Eurome: Uncover Hidden Gems And Timeless Traditions

- Annaawai: Marriage Status And Relationship History Unveiled